European banks won’t deliver a green steel transition alone

Julia Hovenier, Banks and steel project lead, BankTrack

Julia Hovenier, Banks and steel project lead, BankTrack

The steel industry, responsible for 11% of global CO2 emissions, is stalling in its urgently necessary green transition. Governments are relying heavily on private banks to finance the transition, as seen in the EU’s 2025 Steel and Metals Action Plan. But upon closer inspection, European banks are stagnating or backtracking in their individual steel decarbonisation strategies.

In order to support a just transition to fossil free steel, banks must adopt steel decarbonisation strategies that:

-

turn targets into policies that restrict finance for companies building new coal-based steel plants;

-

include policies to end finance for companies developing new metallurgical coal mines; and

-

rule out financing for false solutions through their sustainable finance frameworks.

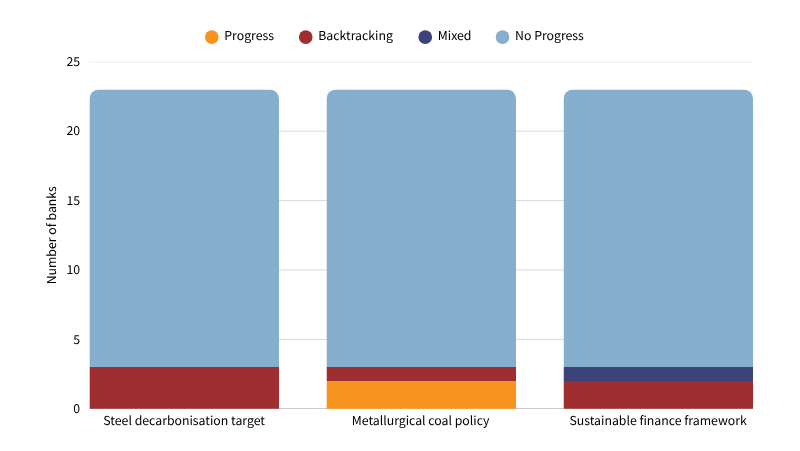

For this article we analysed how 23 European banks' steel decarbonisation strategies changed between 2024 and 2025. We found almost no movement in any of these areas. Where there is change, it’s mostly backtracking. We identified just two examples of progress, both in policies restricting finance for metallurgical coal.

Banks’ steel net zero targets are missing the mark

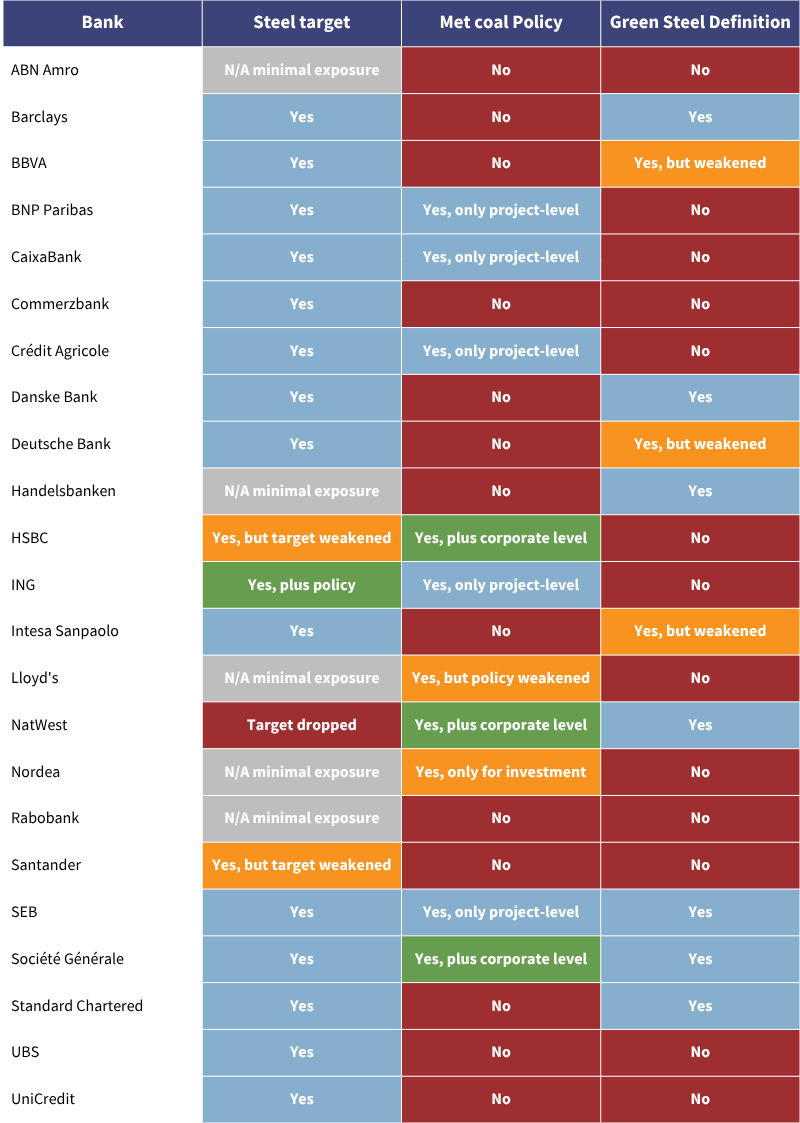

Between 2021 and 2024, 52 global banks set steel decarbonisation targets, including 18 of the European banks analysed here. Target setting was done under the Net Zero Banking Alliance, but after its October 2025 collapse, the future of these commitments was thrown into question. And indeed, between 2024 and 2025, Santander and HSBC quietly weakened their steel targets, while NatWest abandoned its target altogether.

While it’s at least welcome that most banks have maintained their targets in an environment where backtracking is increasingly common, even the existing targets are insufficient to redirect money away from coal-based steel and towards fossil free steel. To date, just one bank, ING, has a policy that restricts finance for blast furnaces, steelmaking technology that cannot operate without coal.

The mix of backtracking and lack of progress on steel targets has real consequences for the industry's decarbonisation. On May 12th this year, HSBC, Santander and Standard Chartered helped steel giant ArcelorMittal raise EUR 1 billion in unrestricted debt, just three weeks after the company abandoned its climate strategy. Continuing to finance this company while it is scaling back its decarbonisation finance, lobbying against critical EU climate policy, and emitting as much CO2 as the nation of Belgium rewards steelmakers actively working against transition.

Still absent: metallurgical coal developers

According to Urgewald’s Metallurgical Coal Exit List, 145 companies are planning new mines as well as expanding existing operations. If realized, these projects would increase global annual met coal production by 52%, when every climate indicator shows coal production should be rapidly decreasing. Yet, the 23 banks analysed here in this blog contributed a total of USD 1.35 billion to metallurgical coal developers between 2021 and 2024.

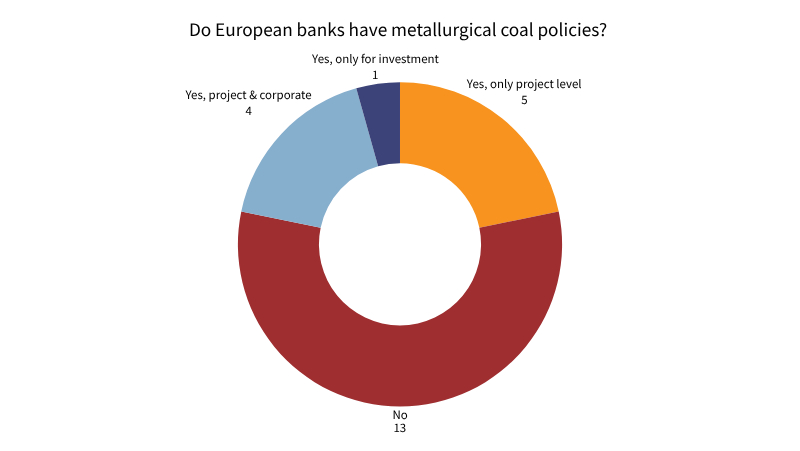

Against this alarming picture, just 10 of the banks analysed have restrictions for metallurgical coal. One bank, Lloyds, has weakened its policy, while two banks, HSBC and NatWest, improved their policies (ironically, the same banks that backtracked on their steel targets). NatWest rightfully removed language about the necessity of metallurgical coal, while HSBC expanded the coverage of its policy to put more scrutiny on corporate finance.

It is undeniable that the adoption of strong metallurgical coal policies in the banking sector isn’t coming fast enough. Importantly, only three banks have restrictions at the client level, and even these are insufficient. Given that only 4.2% of fossil finance is project finance, policies that only cover project finance are clearly not enough.

With this bank policy landscape, it should come as no surprise that several European banks continue to finance Glencore, a company charging ahead with a massive project to build a new mountaintop removal met coal mine in Canada, locking in coal production into the 2060s.

The door remains open for false solutions

Not all solutions in steel decarbonisation are equal. Some risk locking in fossil fuels and driving further harm to people and the environment. For this reason, the EU, and banks, have adopted taxonomies and frameworks to specify which technologies count as “green”. Our research earlier this year found that banks already have weak definitions of “green steel” that allow “green” finance to flow towards false solutions. Unfortunately this analysis found little change.

Deutsche Bank, BBVA and Intesa Sanpaolo all weakened their frameworks to include more false solutions, including Carbon Capture and Storage (CCS) and steelmaking with fossil-based hydrogen and gas. However Intesa Sanpaolo also added steel recycling facilities to its framework, an improvement which gives the bank a mixed record on this overall. It’s worth noting that banks hide behind a weak EU Taxonomy to justify their green steel definitions, which leaves the door open for CCS, biomass, and gas-based steelmaking.

Maintaining weak frameworks on green steel comes with dire consequences, especially for communities in the Global South. In 2025, Intesa Sanpaolo, alongside six other banks, gave Luxembourg-based steel company Ternium a USD 1.25 billion green loan for the construction of a gas-based steel plant in Pesquería, Nuevo León, Mexico. Ternium Mexico claims the new steel plant is sustainable because it will run on gas instead of coal. However, if constructed, this plant would contribute to an industrially-driven public health crisis in Monterrey. Additionally, the project will expand gas infrastructure in Mexico, locking in fossil-fuel usage in the steel industry. Communities in Mexico are calling on European and US banks to prevent this from happening again elsewhere.

Where to from here?

We need finance to flow away from coal-based steel, and towards fossil free steel. Rather than stepping up to the challenge, European banks are stalling, or retreating, with few exceptions. Left to their own devices, European banks could be responsible for an uptick in coal-based steel making, new coal mines, and air pollution from false solutions in Europe, and abroad.

The EU and European governments, including the incoming administration in the UK, have a responsibility to bring their banking sectors in line with a transition to fossil-free steelmaking according to Article 2.1c of the Paris Agreement. They should do so by:

-

setting credit guidance that limits the flow of finance towards new coal-producing/consuming mines and steel plants (i.e. complementing Sustainable Finance taxonomies with a “dirty taxonomy”)

-

revising Sustainable Finance Taxonomies to explicitly exclude false solutions in steel decarbonisation

-

redefining fiscal policy to raise money for a publicly funded and coordinated just transition to fossil free steel

Notes and policy changes:

Overview of progress & backtracking as of July 2026:

Steel targets:

- Backtracking: Santander replaced a -32% intensity reduction target (2019 baseline, 1.07 tonnes of carbon dioxide equivalent per tonne of steel manufactured (tCO₂e/t) by 2030) with a weaker range of -13% to -20% (2023 baseline, 1.17–1.28 tCO₂e/t by 2030);

- Backtracking: HSBC changed its steel target baseline from 2019 to 2023 and raised the 2030 target from 1.05 tCO₂e/t to a range of 1.29–1.52 tCO₂e/t while also descoping aluminium from the combined iron, steel and aluminium target, reducing overall coverage;

- Backtracking: NatWest withdrew all 16 of its SBTi-validated sector targets, including a commitment to reduce iron and steel emissions intensity by 50% per tonne by 2030, replacing them with nine activity-based targets that cover only 61% of its lending book (down from 79%) and have not been submitted for SBTi validation.

Metallurgical coal policies:

- Progress: HSBC strengthened its 2022 metallurgical coal policy by adding an explicit exclusion for new metallurgical coal infrastructure and introducing an enhanced due diligence requirement for any new relationship with a prospective client holding metallurgical coal assets;

- Progress: NatWest introduced a project finance exclusion for new metallurgical coal mines and removed language describing metallurgical coal as "essential" for the steel industry;

- Backtracking: Lloyds narrowed its metallurgical coal client restriction by adding the qualifier "as part of their primary activities", allowing new clients where metallurgical coal mining is not classified as their core business. Any new client with revenues derived from “operating metallurgical coal mines” was excluded under Lloyds’ previous policy.

Steel sustainable finance frameworks:

- Backtracking: BBVA explicitly added CCUS and progressive substitution of coal with gas in reduction stages and thermal processes as “transition activities” for the steel sector to its sustainable finance framework;

- Backtracking: Deutsche Bank updated its Sustainable Finance Framework to now integrate DRI-EAF based on hydrogen, but this is not restricted to green hydrogen, opening the door for fossil-based hydrogen with CCUS.

- Mix: Intesa Sanpaolo updated its Sustainable Lending Framework to include the false solution of carbon capture among the technologies identified to support the decarbonisation (backtracking). And while it also adds “transformative industrial technologies for decarbonisation” such as “scrap-based EAFs or lower-emitting DRIs” (potentially progress), its definition of the latter is unclear and could open the door to false solutions as it is not explicitly restricted to green hydrogen.